My friend Quentin Fottrell is the Moneyologist columnist over at MarketWatch. He recently shared with his facebook group a reader question about whether a woman should help her 75-year-old sister with medical-related credit card debt.

Two commenters asked, “Why does she have medical costs? Isn’t she on Medicare?” They thought that Medicare covered most healthcare costs for older adults.

Unfortunately, this simply isn’t true. While Medicare is the primary health insurer for most older adults, it only pays a part of the healthcare bill. There are three kinds of out-of-pocket costs that we face!

- Monthly Premiums. Medicare premiums (the amount you pay for your health insurance every month) and any premiums you pay for additional coverage to cover cost sharing and the coverage gaps.

- Copayments and Deductibles. This includes deductibles that must be met before Medicare will pay anything, co-payments at the time of service, and the cost of any care that exceeds maximum coverage.

- Services Medicare doesn’t cover. Examples of uncovered services include dental care, hearing aids, glass, or foot care. And, of course, Medicare will NOT pay for any personal care or facility-based services an older adult might need over a long period of time – for help with basic activities like bathing or dressing.

These costs add up differently depending on how much healthcare you need and where you live. We’ve provided the basics below and also created a downloadable cheat sheet for you to use as reference. But the absolute best resource for understanding all of this is Medicare for Dummies by Patricia Barry.

Premiums

If your parent is enrolled in traditional Medicare, the good news is that they most likely won’t pay a premium to enroll in Medicare Part A, which covers hospital and rehab care. But, the bad news is that there are up to three monthly premiums that they will face:

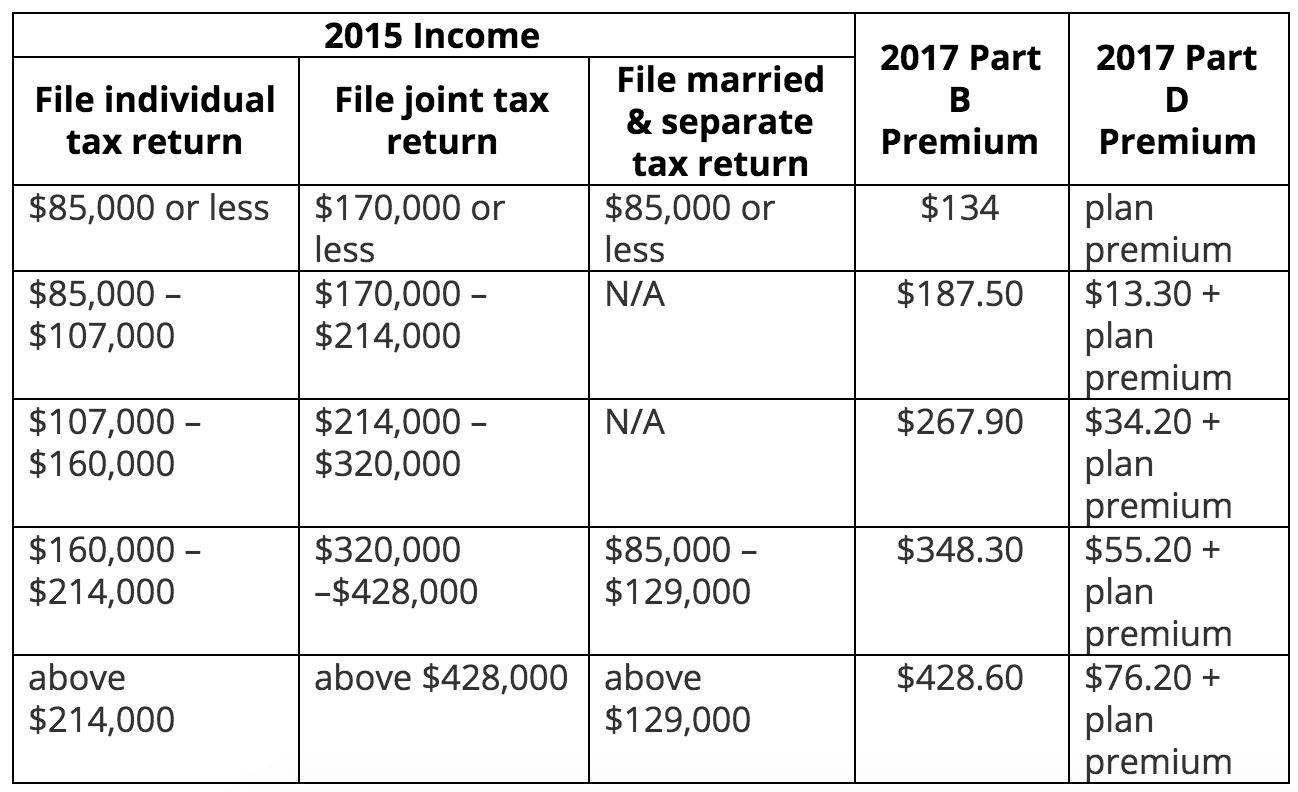

- Medicare Part B premiums—which cover doctor’s services, outpatient care, and medical equipment. These premiums vary by income. The standard amount paid by most seniors in 2017 is $134 per month. Higher-income individuals must pay higher premiums: up to $428.60 per month (see Table below).

- Medicare Part D premiums—which cover prescription drugs. To receive Medicare drug coverage, seniors must buy Part D coverage from a private insurance plan. Premiums vary by plan, and—as with Part B—higher-income individuals must pay an additional premium.

- Medigap (Medicare Supplement Insurance) premiums. This is optional! A lot of people buy additional private insurance to protect them against Medicare cost-sharing and coverage limits. Premiums vary by plan and area.

Here’s an important tip: Make sure your parents sign up for Parts B, D and Medigap within the first six months after turning 65. There are hefty penalties and higher prices to pay if they wait.

(source)

(source)

Deductibles, Copayments, and Coverage Limits

In addition to monthly premiums, Medicare also requires that enrollees pay part of the cost of healthcare at the point of service. Super confusing: these costs also vary by the kind of service being received (evidence of the fact that a bunch of 25-year-old Congressional staffers made up these rules). Many older adults buy Medigap plans to cover some of these costs.

- Hospital stays

- $1,316 deductible per “benefit period” (a period of time that begins the day you’re admitted to the hospital and ends 60 days after discharge) – that is, you could have multiple “benefit periods” and pay the deductible more than once in a year!

- Co-payment: Days 1-60: $0, days 61-90: $329/day, days 91+: $658/day until lifetime coverage limit reached, then all costs.

- Skilled nursing facility (SNF) (Medicare only covers this if you have a qualifying 3 day hospital stay so make sure you aren’t in the hospital for observation if you want a possible SNF stay covered!)

- No deductible

- Co-payment: Days 1-20: $0, Days 21 – 100: $164.50/day, days 101+: all costs

- Home health care

- No deductible or copayment!

- Doctor services, outpatient care (including most emergency room visits), and medical equipment

- Deductible: $183 per year

- Co-insurance: 20%

- Prescription drugs

- Deductibles and copayments vary by plan

Coverage Limits

For some services, there are limits on Medicare coverage, after which you are responsible for all costs. The big ones are the lifetime maximum on hospital days and the limit on SNF days. After 90 days in the hospital in any given benefit period, you can access 60 “lifetime reserve days.” Once these are exhausted, you are responsible for all hospital costs. Similarly, you are limited to 100 SNF days in each benefit period. Hospital lifetime reserve days cannot be used for extra SNF care after day 100.

Additionally, unlike other kinds of insurance plans, Original Medicare does not have out-of-pocket maximum spending limits. This means there is no yearly limit on what you pay out-of-pocket.

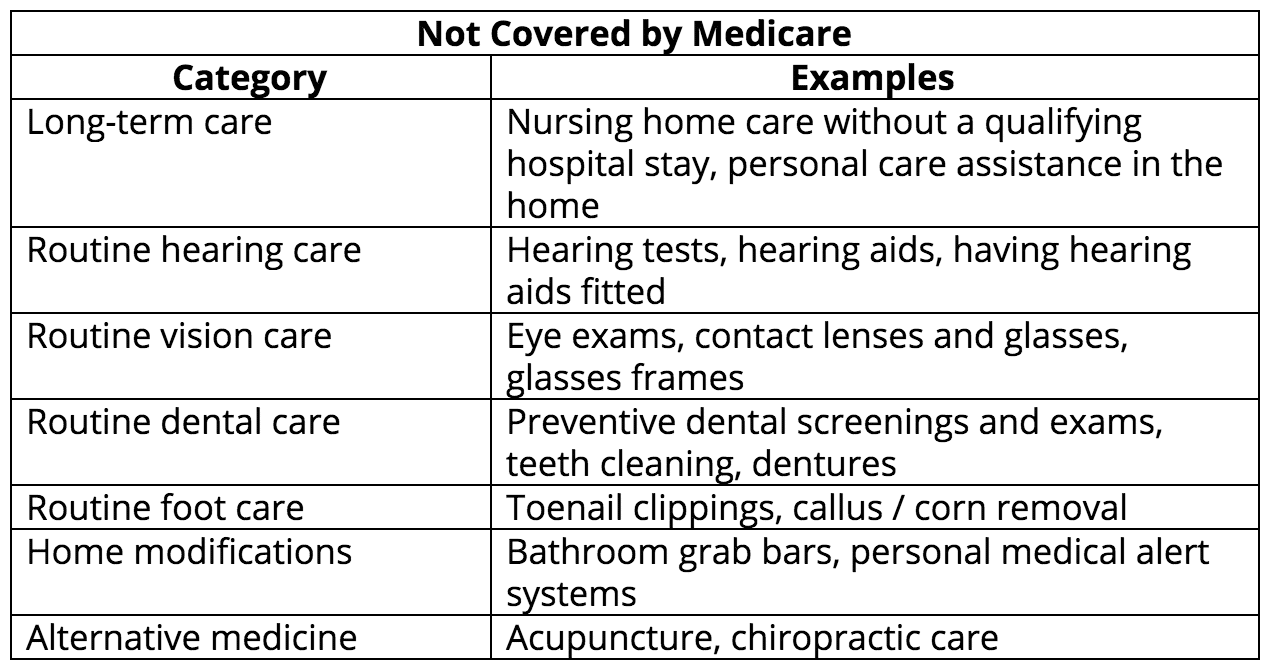

Services Medicare Doesn’t Cover

There are many health care services that Original Medicare doesn’t cover at all. Your parent will be responsible for paying this on their own, or by finding separate insurance coverage.

So what can you do about this?

As the Moneyologist reader relates above, the out-of-pocket costs of Medicare can add up to a substantial financial burden. There are a few ways to protect yourself.

The first thing to do is to see if your parent is eligible for Medicaid, which might help to cover some of these costs for them. Here’s an earlier post that can get you started with Medicaid.

The second option is to purchase a Medigap plan, which will help with Medicare copayments and deductibles. It’s really important to sign up for Medigap during your open enrollment period, which is the first six months you’re enrolled in Medicare after you turn 65. We’ll explore Medigap in more detail in a future blog.

Finally, enrolling in a Medicare Advantage (MA) plan might be a good choice. Some people worry about managed care—that it will mean they have to find a new doctor, or that they’ll be denied important healthcare services. But, MA has a lot of benefits. MA plans are a one-stop shop for all your Medicare benefits: Parts A, B, and D. In some cases, MA plans are less expensive than the Original Medicare premiums, and all plans offer the protection of a yearly out-of-pocket maximum. Finally, a lot of MA plans offer additional benefits like preventive vision and dental care.

This is all really confusing—even for the experts! Let us know in the comments if you have specific questions you’d like us to dig into for a future blog.